December Macro

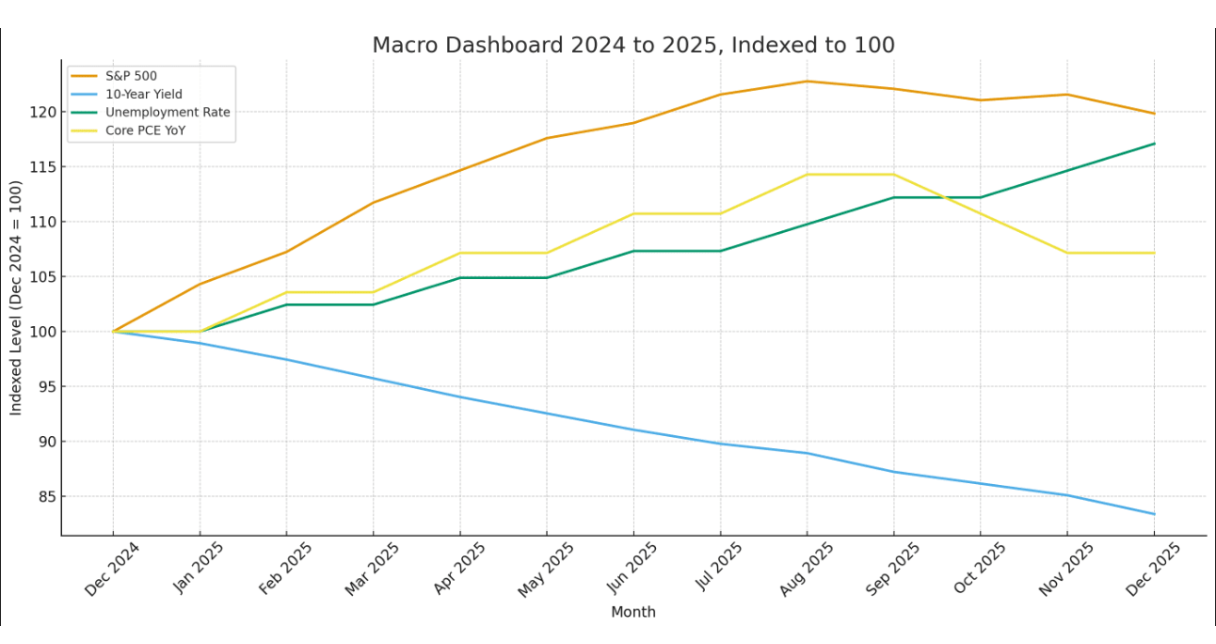

As December 2025 unfolds, the U.S. macro landscape feels like a gathering storm viewed through frosted glass, visible in outline yet blurred by holiday cheer and year end distortions. The labor market’s controlled descent tips into unease as unemployment reaches 4.8 percent and seasonal hiring fails to disguise the chill. Core inflation holds near 3.0 percent on the year, with services inflation still anchored by wage stickiness and tariff passthroughs.

The yield curve has fully uninverted, a technical sigh of relief that hides deeper fiscal fatigue as the FY2025 deficit moves past 2.5 trillion dollars, or 9.1 percent of GDP. The dollar weakens, equities hold onto gains through thin holiday volume, and political winds sharpen ahead of the 2026 midterms. Markets exhale in complacency, the real economy inhales caution. This is transition’s quiet crescendo, a shift from engineered buoyancy to the pull of gravity.

Themes Under Observation

1. Dollar and Global Flows

The dollar continues its subtle erosion. EURUSD rises toward 1.172. The DXY slips below 98, revisiting levels last touched in 2021. Gold holds above 4,500. BRICS central banks expand commodity and yuan based liquidity lines, not as rebellion but as risk management. The world is not abandoning the dollar, it is diversifying away from singular dependence. The old map no longer fits the landscape, so we begin navigating by new stars.

2. Trade and Fiscal Fractures

The November trade deficit widens toward 98 billion dollars. Imports swell with holiday restocking and tariff anticipation. Exports stagnate under global cooling. Fiscal spending grows heavier as the deficit approaches wartime proportions. Protectionism creates motion, not progress. The United States is reshoring inefficiency, not production. We are borrowing vitality from tomorrow to preserve illusions today.

3. Interest Rates and Policy Posture

The Federal Reserve holds rates between 3.75 and 4.00 percent. Futures price three cuts in the first half of 2026. Powell enters the final turn of his tenure as speculation forms around successors. Growth leaning or caution leaning. Long yields soften. The ten year drifts near 3.95. The two year holds 3.62. The curve renormalizes, but the normalization feels like a bridge built on thin ice. Policy can ease, but it cannot erase structural imbalance.

4. Market Structure and Speculative Momentum

Equities end the year with fatigue hidden inside resilience. The S and P closes near 6,950, up seventeen percent year to date. The Nasdaq holds above twenty one thousand. Market breadth sinks below thirty percent. Retail speculation flickers but does not ignite. Bitcoin cools to 112,000 with ETF flows slowing. On chain metrics reveal truth beneath narrative. The final energy of the cycle is nostalgia rather than conviction.

5. Commodities and Energy

Gold steadies around 4,520. Silver trades near 54. Oil drifts between 82 and 87. Supply remains stable while demand softens. Agricultural commodities calm as harvests normalize. Commodities reflect psychology now, they rise when trust fractures and settle when clarity returns.

Economic Data

Labor Market

Payrolls add a modest 22,000. Unemployment reaches 4.8 percent. Prior month revisions subtract another 89,000. Participation drops to 62.4 percent. The descent continues with a tired rhythm. Not a crisis, but a controlled cool down. Healthcare holds, energy steadies, manufacturing frays, services soften, retail contracts. This is an economy catching its breath after moving too quickly for too long.

Inflation Metrics

Core CPI holds at 3.3 percent year over year. Services inflation remains firm. Energy passthroughs lift the monthly print. Core PCE holds at 3.0 percent. Tariffs embed themselves deeper. Inflation shifts from fire to ember. It does not burn out of control, nor does it extinguish. It simply endures.

Silver Lining

Despite the December fade and the quiet strain beneath the surface, the real silver lining is that the system is rebalancing rather than breaking. The softening in the labor market, the steady downtrend in long term yields, and the plateau in inflation show an economy releasing pressure in a controlled way rather than collapsing under it. Bonds signal confidence that the Federal Reserve will soon have room to ease, credit conditions will loosen, and liquidity will return without triggering financial stress.

Equities, still up nearly twenty percent on the year, reveal that adaptability is being rewarded even as growth slows. This is what a soft landing feels like, an uneasy deceleration that creates the conditions for the next expansion. The silver lining is that the discomfort is the adjustment, the cooling that prevents a fracture, and the quiet pause that allows momentum to rebuild.

Interpretation and Positioning

This month is erosion, slow and deliberate, unromantic pressure shaping the next chapter. Real yields compress, fiscal anchors weaken, and political gravity strengthens. Liquidity supports markets, but structure and flow begin to diverge. The wise builder shifts from aggression to coherence.

Hold what earns. Release what depends solely on narrative. Keep structures modular and hedged. Stay liquid enough to move, not liquid enough to freeze. In turbulence, liquidity becomes choice, not fear. Durability is strategy now. Not speed or prediction, but presence.

Bottom Line

December reveals the truth that whispered all year. The system is functional but frayed, markets trade belief, households trade caution, and policy trades time. Direction matters less than depth. Pace matters less than posture. The true north of this phase is durability.

Systems Insight

Late cycle dynamics mirror human psychology. We reach for light even as shadows lengthen. We cling to ascent even as altitude demands humility. Divergence between markets and the real economy is not dysfunction, it is the human story reflected in data.

This is a month for reflection.

Your task is to listen.

This is a month for reflection:

Your task is to listen.

The Quiet Freeze

The year ends with the feeling of air turning cold, not with panic but with clarity. Markets no longer run on adrenaline, the labor market stops pretending it is invincible, and yields begin their slow descent toward relief.

This is the quiet freeze that settles in before a new season, the moment when excess heat drains from the system and the real structure underneath is revealed. It is not collapse, it is coherence returning. The slowdown is deliberate, the cooling intentional, the equilibrium resetting itself. In this stillness, the next cycle gathers strength, waiting for the world to recognize that winter is not an ending, it is preparation.